Tuesday, August 25, 2009

Science: Prediction or Explanation?

Economist's View: "There has been no shortage of effort devoted to predicting earthquakes, yet we still can't see them coming far enough in advance to move people to safety. When a big earthquake hits, it is a surprise. We may be able to look at the data after the fact and see that certain stresses were building, so it looks like we should have known an earthquake was going to occur at any moment, but these sorts of retrospective analyses have not allowed us to predict the next one. The exact timing and location is always a surprise."

Monday, August 17, 2009

Felix Salmon » Blog Archive » Chart of the Day: The stock market’s P/E Ratio | Blogs |

Felix Salmon - The stock market’s P/E Ratio:

See the chart at the link. However, the main reason that P/E is high is not that prices are high, it is that earnings are unusually low. In the absence of bubble psychology, prices should stay fairly stable since they are the forecasts of future earnings streams, but earnings are certainly very volatile. Thus, the P/E should fluctuate during recessions and really ought to be higher during downturns than it is during booms.

"Stocks are now trading at p/e ratios not seen since 2004. This is more than pricing in a recovery — this looks very much like pricing in a return to the status quo ante. Does anybody really still think that corporate profits are going to be able to rise faster than US GDP indefinitely? It seems from the level of the stock market that, yes, they do."

See the chart at the link. However, the main reason that P/E is high is not that prices are high, it is that earnings are unusually low. In the absence of bubble psychology, prices should stay fairly stable since they are the forecasts of future earnings streams, but earnings are certainly very volatile. Thus, the P/E should fluctuate during recessions and really ought to be higher during downturns than it is during booms.

Saturday, August 15, 2009

More on deficits and interest rates (wonkish) - Paul Krugman Blog - NYTimes.com

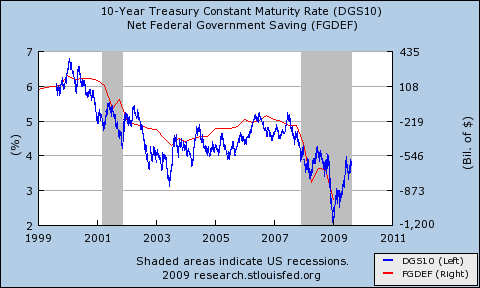

More on deficits and interest rates (wonkish) - Paul Krugman Blog - NYTimes.com: "I noted that over the past decade there has been a close negative correlation between deficits and interest rates:"

This is the exact opposite of what macroeconomics textbooks teach. If there is deficit spending, the net national savings rate tends to go down and the interest rate goes up (as in the standard savings and investment graph). That is true during economic growth. However, during a recession, there is excess savings because consumers try to save more and firms tend to invest a lot less and that makes the interest rate drop (again as the standard savings and investment graph would predict). The reason is that short-run deficit fluctuations are caused by the automatic stabilizers (tax revenues automatically decline and government spending automatically increases)

Read the whole thing.

This is the exact opposite of what macroeconomics textbooks teach. If there is deficit spending, the net national savings rate tends to go down and the interest rate goes up (as in the standard savings and investment graph). That is true during economic growth. However, during a recession, there is excess savings because consumers try to save more and firms tend to invest a lot less and that makes the interest rate drop (again as the standard savings and investment graph would predict). The reason is that short-run deficit fluctuations are caused by the automatic stabilizers (tax revenues automatically decline and government spending automatically increases)

Read the whole thing.

Monday, August 10, 2009

Global Development: Views from the Center » Blog Archive » Crisis? Not If We Take a Long View (Development Impacts of Financial Crisis)

Global Development: Views from the Center » Blog Archive » Crisis? Not If We Take a Long View (Development Impacts of Financial Crisis): "When you’re done reading today’s news stories about the crisis, take a deep breath. Media coverage is focused on the very short term, as usual. Speculation abounds that we live in a different world now. I’m reminded of portentous claims after the Asian Financial Crisis that “the miracle was over”, claims which look very overwrought in hindsight. In historical perspective, many of the most worrisome recent crises are small bumps on a very long road."

Grasping Reality with Both Hands

Grasping Reality with Both Hands: "Why Aren't We Undergoing Another Great Depression?

Paul Krugman: "The answer, basically, is Big Government...."

Paul Krugman: "The answer, basically, is Big Government...."

The loose end in Krugman's article is why there weren't more Great Depressions back in the old days, before big government. The answers, I think, are two:

Business cycles are a disease of the post-agricultural economy--of the nonfarm economy. If you look back at the nonfarm unemployment rate before 1930, things look not as bad as the Great Depression but still pretty bad.

Most countries had a form of "big government"--a military large in size relative to its nonfarm economy and an activist, interventionist central bank--reaching far back into the past.

Chart: The Collapse In Global Trade - Planet Money Blog : NPR

Chart: The Collapse In Global Trade - Planet Money Blog : NPR: "The chart above shows that we're living through the only major, sustained fall in global trade since 1970. ..."Behind each story lies a catastrophic decline in gross exports," Weinberg writes. The IMF data on exports track a 36 percent fall from the peak of $1.5 trillion in July 2008. "We have never experienced anything like this in our lifetimes. Neither, quite frankly, did we ever think we would."

Wednesday, August 5, 2009

Marginal Revolution: Identifying and Popping Bubbles: Evidence from Experiments

Marginal Revolution: Identifying and Popping Bubbles: Evidence from Experiments: "On the way up, bubbles encourage excessive investment in the bubble sector. On the way down a bursting bubble can create wealth shocks, liquidity shortages, and balance-sheet death-spirals. For both of these reasons, it would be good to be able to identify and pop bubbles. Identifying bubbles isn't easy, however, because, especially when interest rates are low, prices can increase rapidly with small, rational changes in investor expectations. But the difficulty of identifying bubbles is reasonably well known. What I think may be less appreciated is that bubbles are hard to pop even when you know that they exist."

If we can't identify them and we can't pop them, then we better create institutions that make them less dangerous.

If we can't identify them and we can't pop them, then we better create institutions that make them less dangerous.

Subscribe to:

Posts (Atom)